Your Guide to Confident Homeownership: A First-Time Buyer's Blueprint

Introduction: Navigating Your Path to Homeownership

Welcome to your comprehensive guide to buying your first home. This document is designed to demystify the homebuying process, transforming what can often feel like an overwhelming and anxious experience into a clear, manageable journey. We will provide a step-by-step blueprint that illuminates the path from initial financial preparation all the way to the moment you receive the keys to your new home.

This guide is structured around the five key phases of the homebuying journey, ensuring you have the right information at the right time:

- Financial Foundation: Establishing the bedrock of your purchasing power.

- Assembling Your Team & Strategy: Securing your financing and expert guidance.

- The Home Search: Finding the right property and location.

- The Transaction: Navigating the critical steps from offer to closing.

- Life as a Homeowner: Understanding your new financial responsibilities.

Ultimately, thorough preparation is the key to a successful and satisfying home purchase. This guide will empower you with the knowledge and confidence needed to make informed decisions at every turn, ensuring your first home is a source of stability and pride for years to come.

--------------------------------------------------------------------------------

Phase 1: Building Your Financial Foundation

Financial readiness is the non-negotiable first step in the homebuying process. Before you begin browsing listings or dreaming of paint colors, it is essential to build a solid financial base. A strong foundation not only determines your purchasing power but also ensures long-term stability, helping you avoid the common and stressful mistake of becoming "house poor."

Strengthening Your Credit Profile

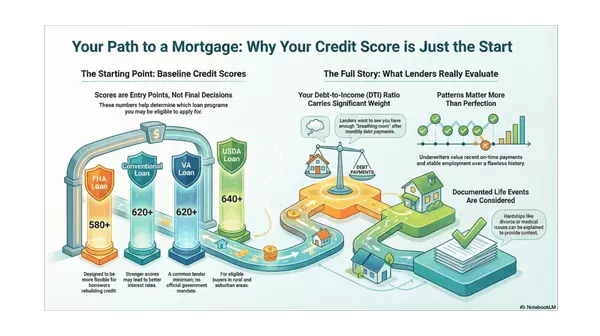

Your credit score is a critical factor that lenders use to determine your eligibility for a loan and the interest rate you will receive. A higher score demonstrates financial responsibility and can save you tens of thousands of dollars over the life of your loan. Lenders typically look for a score of 680 or higher, with scores of 740+ securing the best interest rates.

To build a stronger credit profile, focus on these key actions:

- Pull your credit reports from all three major bureaus to check for errors or discrepancies.

- Pay down high-interest debt, such as credit card balances, to lower your debt-to-income ratio.

- Avoid opening new lines of credit or financing major purchases in the months leading up to your home purchase.

Building Your Cash Reserves

Beyond your credit score, you will need significant cash on hand to complete your home purchase. These savings fall into three essential categories:

- Down Payment: This is the initial portion of the purchase price you pay upfront. While 20% is the traditional figure to avoid private mortgage insurance (PMI), down payments typically fall in the 3-20% range, and some government-backed programs allow for even less.

- Closing Costs: These are the fees associated with finalizing the real estate transaction, including lender fees, title insurance, and appraisal costs. You should budget approximately 2-5% of the home's purchase price for these expenses.

- Emergency Fund: This is a crucial safety net of 3-6 months of living expenses. It provides a buffer for unexpected repairs or life events after you move in. Skipping this step is what often leads to becoming "house poor"—a situation the source material identifies as the #1 mistake first-time buyers make.

Defining Your True Affordability

There is a critical difference between the maximum loan amount a lender will approve and the monthly payment you can comfortably afford. Lenders approve based on formulas that may not account for your personal spending habits or savings goals. A safer, more conservative approach is to determine your own budget first.

A reliable rule of thumb is to ensure your total housing costs do not exceed 25–30% of your gross monthly income. This calculation must include all related expenses:

- Mortgage (Principal & Interest)

- Property taxes

- Homeowners insurance

- HOA fees (if applicable)

- Maintenance (budget approximately 1% of the home's value annually)

With your finances organized and your true affordability defined, you are now prepared for the next logical step: securing your mortgage pre-approval.

--------------------------------------------------------------------------------

Phase 2: Assembling Your Team & Strategy

This pre-search phase is where you transition from planning to action. By securing your financing and enlisting expert guidance, you establish yourself as a serious contender in the housing market, ready to move decisively when you find the right home.

Securing Your Pre-Approval: Your Ticket to the Market

A mortgage pre-approval is a formal commitment from a lender stating that you are approved to borrow a specific amount of money at a particular interest rate. This is a far more powerful credential than a pre-qualification, which is merely an estimate of your borrowing capacity. Getting pre-approved before you start touring homes is essential for three primary reasons:

- It shows sellers you’re serious and have the financial backing to complete a purchase.

- It locks in your buying power by defining a clear and realistic budget.

- It helps you move fast and make a competitive offer immediately in a fast-paced market.

Evaluating Your Loan Options

Many first-time buyers are unaware of the variety of loan programs available, some of which are designed specifically to make homeownership more accessible. It is crucial to explore all options with your lender. Common loan types include:

- Conventional Loan: Often requires a down payment of 3-5% or more.

- FHA Loan: Backed by the government, this loan allows for a 3.5% down payment and may have more flexible credit requirements.

- VA Loan: Available to eligible veterans, service members, and surviving spouses, often requiring 0% down.

- USDA Loan: Designed for rural and some suburban homebuyers, this loan may also require 0% down.

Beyond these primary loan types, be sure to inquire directly with your lender about state or local first-time buyer grants and down payment assistance programs, as these can provide significant financial help.

Choosing Your Real Estate Agent

A great real estate agent is much more than a salesperson; they are your advocate, guide, and protector throughout the entire transaction. They provide the expertise and market insight necessary to navigate complex negotiations and avoid potential pitfalls.

Key Strengths of a Great Agent

- Deep local market knowledge to help you find value and avoid overpriced properties.

- Clear communication skills to explain contracts and processes in an understandable way.

- Strong negotiation skills to advocate for your best interests.

- Protective instincts to warn you when a house might be a bad long-term investment.

A great agent protects you; a bad one can cost you. Be vigilant for these red flags and be prepared to end the relationship if you see them:

Warning Signs to Watch For

- Pressure tactics to make a quick decision or offer more than you are comfortable with.

- Poor communication or being difficult to reach.

- Ignoring your budget and consistently showing you homes outside your price range.

With your pre-approval in hand and a trusted agent by your side, you are fully equipped to begin the active process of finding your new home.

--------------------------------------------------------------------------------

Phase 3: The Search - Finding the Right Home & Location

The home search is a unique blend of disciplined, logical planning and emotional awareness. A successful search begins with separating your core needs from your wants before you start viewing properties. This discipline ensures that your final decision is based on a solid foundation, not just the fleeting excitement of a beautiful kitchen or a finished basement.

Defining Your Priorities: Must-Haves vs. Nice-to-Haves

Creating a clear list of your non-negotiable requirements versus desirable features is a crucial strategic step. This list becomes your anchor, preventing impulse decisions when emotions are running high during home tours. It allows you to evaluate each property objectively against your predetermined criteria.

|

Must-Haves |

Nice-to-Haves |

|

Specific number of bedrooms |

Updated kitchen |

|

Maximum commute limit |

Finished basement |

|

Yard or dedicated parking |

Fireplace |

|

Feeling of safety in the area |

|

Due Diligence on the Location

Remember, you are not just buying a structure; you are buying a permanent place in a specific location. The neighborhood and its characteristics will impact your daily life and the long-term value of your investment just as much as the house itself. Thorough research is non-negotiable.

Your Neighborhood Investigation Checklist

- Commute Times: Check travel times to work and other important locations during peak rush hour, not just on a weekend.

- Property Tax Rates: Research the local property tax rates, as they can significantly impact your monthly housing costs.

- School Districts: Even if you do not have children, the quality of local schools has a major impact on resale value and the overall stability of the neighborhood.

- Crime Trends: Review local crime statistics to ensure you feel safe and comfortable.

- Planned Developments: Look into any major construction or zoning changes planned for the area that could affect traffic, noise, or property values.

Finally, nothing replaces firsthand experience. Make a point to visit the neighborhood at different times—morning, evening, and on the weekend—to get a true feel for the community's rhythm and atmosphere.

Once you find a home in a location that meets your criteria, you are ready to move on to the next step: making an offer and entering the contract phase.

--------------------------------------------------------------------------------

Phase 4: From Offer to Keys - Navigating the Transaction

This phase marks the point where the process becomes formal and legally binding. It is a period that requires careful attention to detail, strict adherence to deadlines, and constant communication with your real estate agent and lender.

Making a Competitive Offer & Negotiation

A compelling offer is about more than just the price. It is a comprehensive package that includes key terms designed to protect you and signal your seriousness to the seller. With your agent's guidance, your offer will include:

- Contingencies: These are clauses that allow you to back out of the deal without penalty if certain conditions aren't met. Standard contingencies include the home inspection, your ability to secure financing, and the property appraising for at least the purchase price.

- Earnest Money: This is a deposit made to the seller to demonstrate your commitment. It is typically held in escrow and applied toward your down payment at closing.

The Home Inspection: Your Most Important Safeguard

The home inspection is a critical step that provides an in-depth, objective assessment of the property's condition. Never waive the home inspection unless you fully understand the significant financial risks involved. A professional inspection serves three critical functions:

- It can save you thousands by uncovering hidden defects before you buy.

- It provides negotiation leverage to ask the seller for repairs or credits.

- It offers an exit from a bad deal if major structural or system-wide issues are discovered.

Final Steps to the Closing Table

After the inspection and negotiation periods are complete, several final tasks must be accomplished to reach the closing table. Following this sequence will ensure a smooth conclusion to your transaction:

- Secure Homeowners Insurance: You will need to provide proof of an active insurance policy to your lender before they will fund the loan.

- Lock Your Mortgage Rate: Work with your lender to lock in your interest rate, protecting you from market fluctuations before closing.

- Review the Closing Disclosure: This document outlines all final loan terms and costs. By law, you must receive it at least three business days before closing, giving you ample time to compare it with your initial Loan Estimate and address any discrepancies with your lender.

- Conduct the Final Walkthrough: Shortly before closing, you will walk through the property one last time to ensure it is in the agreed-upon condition and that any negotiated repairs have been completed.

- Prepare Certified Funds: You will need a cashier's check or wire transfer for your down payment and closing costs.

The Mindset for Success

The homebuying process can be an emotional rollercoaster. It is vital to remain mentally prepared to walk away if a deal doesn't feel right. The goal is not just to buy a house, but to buy the right house for you. The right house is one that:

- Fits your budget comfortably.

- Meets your essential needs.

- Doesn’t give you anxiety about the financial commitment.

If a property fails to meet these criteria, have the confidence to walk away. Trust your judgment and have the discipline to walk away. The right opportunity will not require you to compromise on your core financial and personal needs.

Following a successful closing, you will transition from homebuyer to homeowner, bringing a new set of responsibilities.

--------------------------------------------------------------------------------

Phase 5: Life as a Homeowner - Understanding the True Costs

The moment you receive the keys, your financial responsibilities shift significantly. The true cost of homeownership extends far beyond the monthly mortgage payment, and proactive budgeting for these additional expenses is essential for long-term financial health and peace of mind.

The Hidden Costs of Homeownership

Renting does not prepare you for the variety of expenses that are solely your responsibility as a homeowner. Being aware of these "hidden costs" allows you to plan for them from day one.

- Repairs: From a new roof to a failing HVAC system or a broken appliance, you are responsible for the full cost of repairs and replacements.

- Higher Utilities: Larger spaces often come with higher bills for electricity, gas, and water than you may have experienced in a smaller rental unit.

- Landscaping & Snow Removal: Maintaining your yard, trees, and driveway is an ongoing cost, whether you do it yourself or hire a service.

- HOA Special Assessments: If you live in a community with a homeowners association, you may be subject to occasional large, one-time fees (special assessments) for major community repairs like paving roads or replacing roofs.

- Property Tax Increases: Property taxes are not fixed and can rise over time based on local government budgets and reassessments of your home's value.

To avoid financial stress, it is critical to plan for maintenance from the very beginning. One of the most common mistakes first-time buyers make is "Draining all savings at closing." By preserving your emergency fund and establishing a separate, ongoing savings fund specifically for home maintenance and repairs, you can confidently manage the true costs of homeownership.

--------------------------------------------------------------------------------

Appendix A: Month-by-Month Homebuying Timeline

This timeline provides a general overview of the homebuying process. The average duration for a first-time buyer is 4-6 months, but this can vary significantly based on your market and personal circumstances.

Month 1 – Financial Setup & Education

- What's happening: Credit review and budgeting, learning loan options, researching neighborhoods.

- Your focus: Fix credit issues, build a savings plan, avoid major purchases.

Month 2 – Pre-Approval & Agent Selection

- What's happening: Lender pre-approval, choosing a real estate agent.

- Your focus: Compare lenders, lock in a realistic budget, define your must-haves.

🚫 Don’t open new credit or finance anything.

Month 3 – House Hunting

- What's happening: Touring homes, narrowing down neighborhoods, experiencing emotional highs and lows (this is normal).

- Your focus: Stay within your budget, avoid "stretching" for upgrades you can't afford, be patient.

Month 4 – Offer & Contract

- What's happening: Making offers, engaging in negotiations, going under contract.

- Your focus: Protect your contingencies, understand all deadlines, submit earnest money promptly.

Month 5 – Inspection, Appraisal & Loan Processing

- What's happening: Home inspection, appraisal ordered by the lender, underwriting review of your finances.

- Your focus: Negotiate repairs if needed, submit all requested documents quickly.

Don’t change jobs or income during this critical period.

Month 6 – Closing & Move-In 🎉

- What's happening: Final walkthrough, signing closing paperwork, getting the keys.

- Your focus: Review the Closing Disclosure carefully, bring certified funds, set up utilities, and change your address.

--------------------------------------------------------------------------------

Appendix B: Comprehensive First-Time Homebuyer Checklist

Use this checklist as a practical tool to track your progress throughout the entire homebuying journey and ensure no critical steps are missed.

🧾 Financial Prep

- [ ] Pull credit reports & correct errors

- [ ] Improve credit score (pay down cards, avoid new debt)

- [ ] Calculate a comfortable monthly payment

- [ ] Save for:

- Down payment

- Closing costs (2–5%)

- Emergency fund (3–6 months)

🏦 Mortgage Prep

- [ ] Research loan types (Conventional, FHA, VA, USDA)

- [ ] Compare at least 2–3 lenders

- [ ] Get pre-approved (not just pre-qualified)

- [ ] Ask about first-time buyer grants or assistance

🏘️ Home Search Prep

- [ ] Choose a trusted real estate agent

- [ ] Define must-haves vs. nice-to-haves

- [ ] Research neighborhoods

- [ ] Set max purchase price & walk-away number

📝 Offer & Contract

- [ ] Understand contingencies (inspection, financing, appraisal)

- [ ] Make offer with agent guidance

- [ ] Negotiate repairs or credits

- [ ] Deposit earnest money

🛠️ Inspection & Due Diligence

- [ ] Schedule home inspection

- [ ] Review inspection report

- [ ] Request repairs or renegotiate

- [ ] Review HOA rules (if applicable)

🧠 Final Steps Before Closing

- [ ] Secure homeowners insurance

- [ ] Lock mortgage rate

- [ ] Review Closing Disclosure

- [ ] Final walkthrough

- [ ] Bring funds to close

Categories

Recent Posts

Agent | License ID: SL3584145

+1(240) 695-2907 | callseansherrie@gmail.com